Chapter 17

Oil Prices

How oil prices work: WTI, Brent, Dubai benchmarks, price reporting agencies, netback pricing, and what drives crude oil prices.

Physical Oil Trading

Wholesale oil trades through two types of contracts: term supply contracts (pre-arranged deliveries at scheduled dates, the majority of physical trade) and spot supply contracts (immediate delivery to the highest bidder). Spot prices reflect real-time supply and demand conditions and anchor virtually all oil pricing worldwide.

Benchmark Pricing

Until the 1980s, oil prices were set by fiat: major oil companies or OPEC producers declared a fixed price that held for weeks or months. Since the mid-1980s, nearly all oil pricing uses benchmarks, with term supply contracts referencing daily spot prices from futures exchanges or trade journals.

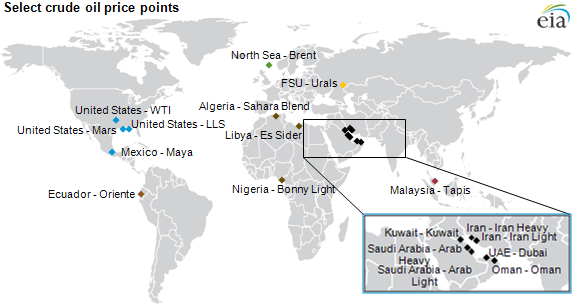

The two primary futures benchmarks are NYMEX WTI (West Texas Intermediate, traded in New York) and ICE Brent (traded in London). WTI prices roughly one-third of the world's oil; Brent prices the other two-thirds. Trade journals like Platts (now S&P Global Commodity Insights) publish daily assessments of over 100 benchmark grades based on OTC (over-the-counter) market activity.

Even OPEC producers use benchmark formula pricing. Each producer sets an Official Selling Price (OSP) as a premium or discount to a benchmark, revised monthly. For example, Nigerian Bonny Light might be priced at Platts Dated Brent plus or minus a differential that reflects quality differences and relative demand.

Table 17-1: Global Crude Oil Benchmarks (2026)

| Benchmark | Region | Venue | Role |

|---|---|---|---|

| WTI | Cushing, Oklahoma | NYMEX (CME) | US light sweet benchmark; physical delivery at Cushing |

| WTI Houston / MEH | US Gulf Coast | NYMEX, Argus AGS | Waterborne US export benchmark, priced FOB Houston |

| Brent (BFOETM) | North Sea + US Gulf | ICE Futures Europe | Global benchmark; BFOETM basket includes Brent, Forties, Oseberg, Ekofisk, Troll, WTI Midland (2023) |

| Dated Brent | North Sea | Platts assessment | Physical cargo benchmark used to price most non-US international crude |

| Murban | Abu Dhabi (UAE) | ICE Futures Abu Dhabi (IFAD) | Launched March 2021; physically delivered Middle East light sour benchmark |

| Dubai / Oman | Middle East | Platts MOC, DME (Oman) | Core Asia-bound Middle East sour benchmark |

| ESPO | Kozmino, Russia | Platts assessment | Pacific Russian medium sour; rose after 2022 sanctions diverted Urals |

| ASCI | US Gulf Coast | Argus assessment | Argus Sour Crude Index; used by Saudi Aramco for US-bound sour cargoes |

Table 17-2: Refined Product Futures Benchmarks

| Contract | Venue | Specification |

|---|---|---|

| RBOB Gasoline | NYMEX (CME) | US gasoline blendstock, NY Harbor delivery |

| NY Harbor ULSD | NYMEX (CME) | Ultra-low sulfur diesel; replaced the legacy heating oil contract in 2013 |

| ICE Low Sulphur Gasoil | ICE Futures Europe | European diesel/heating oil benchmark, ARA delivery |

| Singapore Gasoil 10ppm | Platts MOC, ICE | Asian middle distillate benchmark |

| Marine Fuel 0.5% (VLSFO) | Platts, CME | Bunker fuel benchmark introduced for IMO 2020 sulfur cap |

Front-month WTI has traded between roughly $20 and $145 per barrel since 2007. The 2008 spike, the 2014 to 2016 shale versus OPEC price war, the April 20, 2020 negative print during the pandemic demand collapse, the 2022 Russia-Ukraine spike above $120, and the range-bound $65 to $90 environment of 2024 to 2026 all make the same point: oil is costly to store, supply takes years to adjust, and short-run demand is inelastic, so prices are structurally volatile.

The Delivery-Chain Price Ladder

When physical oil prices are quoted, they are always quoted against a specific point in the delivery chain. Crude accounts for most of the eventual retail price, but each step in the refining and transportation chain adds its own margin. The names of the price points form a ladder. Not every grade follows every rung, and the order can vary, but the sequence below is the canonical framework.

From Wellhead to Retail: US vs EU

| Step | US price | EU price |

|---|---|---|

| Wellhead | $65/bbl | $70/bbl |

| Cargo FOB | $70/bbl | $73/bbl |

| Refinery gate | $73/bbl | $76/bbl |

| Rack (wholesale) | $2.05/gal | $2.15/gal |

| Dealer tank wagon | $2.30/gal | $2.40/gal |

| Retail (pre-tax) | $2.55/gal | $2.70/gal |

| Retail (all-in) | $3.45/gal | $6.50/gal |

| Tax per gallon | $0.90/gal | $3.80/gal |

Illustrative 2024-2025 averages. US = WTI-based, EU = Brent-based. Click toggle to switch units.

Unit Conversions

Oil at retail is sold in US gallons or liters, but wholesale oil trades in barrels, gallons, and metric tonnes depending on the region and the product. The conversion from metric tonnes to barrels depends on density: lighter products pack more barrels per metric tonne than heavier products. The table below gives the canonical factors and the conventional trading units by region. A few fixed relationships are always true: 42 US gallons equal one barrel, one US gallon is roughly 3.785 liters, and one barrel is roughly 159 liters or 0.159 cubic metres.

Table 17-3: Oil Market Units and Conversions

| Product | Region | Traded unit | Bbl per metric tonne |

|---|---|---|---|

| Crude oil (WTI) | Worldwide | bbl | 7.50 |

| Crude oil (Maya, heavy) | Worldwide | bbl | 6.50 |

| Gasoil / diesel / heating oil | Asia | bbl | 7.45 |

| Gasoil / diesel / heating oil | Europe | metric tonne | 7.45 |

| Gasoil / diesel / heating oil | US | US gallon | (gal only) |

| Jet fuel / kerosene | Asia | bbl | 7.88 |

| Jet fuel / kerosene | Europe | metric tonne | 7.88 |

| Gasoline | Asia | bbl | 8.33 |

| Gasoline | Europe | metric tonne | 8.33 |

| Naphtha | Europe | metric tonne | 8.90 |

| Residual fuel oil | Asia / Europe | metric tonne | 6.40 |

The barrels-per-tonne factor matters when a trader negotiates a swap: a Brent-based crude swap in Europe typically settles in dollars per barrel even though the physical cargo is measured in metric tonnes. A slightly wrong conversion factor (say, 7.58 when the right number is 7.45) compounds across millions of tonnes and can reconcile to millions of dollars over a year.

Formula Pricing: A Worked Example

Nearly all crude oil sold into the international market today is priced using a formula that references one or more published benchmarks. The formula accounts for quality differences (light vs heavy, sweet vs sour, waxy vs clean), for location differences (delivered price at the refinery gate vs loaded FOB at the export terminal), and for a residual premium or discount (the Official Selling Price, or OSP) that the producer revises monthly. The Saudi Aramco OSP announcement on the tenth of every month is one of the most watched events in the physical market.

The clearest published example is Mexico's PEMEX, which prices its three flagship crude grades against combinations of four benchmarks using publicly disclosed formulas. The formulas below are the canonical 1990s-2000s versions; the exact weights and the constant term change over time, but the structure has been stable for thirty years. WTS is West Texas Sour, LLS is Light Louisiana Sweet, Dated Brent is the Platts North Sea assessment, and US Gulf No. 6 3% is a heavy high-sulphur residual fuel oil assessment.

Table 17-4: Mexican PEMEX Crude Formulas (illustrative)

| Grade | API | Formula |

|---|---|---|

| Olmeca (light) | 39° | 0.333 × (WTS + LLS + Dated Brent) + constant |

| Isthmus (medium) | 33° | 0.4 × (WTS + LLS) + 0.2 × Dated Brent + constant |

| Maya (heavy sour) | 22° | 0.4 × (WTS + US Gulf No.6 3%) + 0.10 × (LLS + Dated Brent) + constant |

Read the Maya formula carefully: a heavy sour crude is priced not against a single crude benchmark, but against a blend of a sour crude (WTS), a residual fuel oil (US Gulf No.6 3%), and two light sweet crude benchmarks (LLS and Dated Brent). The weights reflect what a complex refinery would actually pay for the constituent yield: heavy sour crude is really a blend of light transport fuel potential and bottom-of-the-barrel residual potential, and Maya is priced as exactly that blend. The constant term is PEMEX's monthly OSP adjustment. It moves with demand for Maya in Asia and the US Gulf and with the refining margin offered by US coking refineries, which are the natural buyer.

Most non-OPEC producers price their crude with similar formulas. OPEC producers use them too: Saudi Aramco's Arab Light OSP to Asia is priced as a differential to the average of Oman and Dubai, while Arab Light OSP to the US Gulf is priced as a differential to ASCI. The same physical cargo is therefore priced against completely different benchmarks depending on which destination buyer is on the other side.

Freight Netback Pricing

A variation of formula pricing is freight netback pricing, used when there is no liquid benchmark at the actual pricing location. The seller takes a published benchmark price at a different location, subtracts the cost of shipping oil from that location to the pricing location (or adds it, if flowing the other way), and uses the result as the netback price. The freight leg references a published benchmark such as the Baltic Exchange tanker rate or a Platts freight assessment. Freight netback pricing is common for obscure loading ports, for landlocked pipeline points, and for spot cargoes that have to be diverted mid-voyage. It is also the basis for arbitrage decisions: a cargo will only move from point A to point B if the freight cost is less than the price difference between A and B.

Pricing Windows and the Platts MOC

The price a Platts assessment publishes at the end of a trading day is not the last observed trade: it is the value of the market at the close, estimated from a narrow window of tightly observed spot activity. The window is called the Market on Close (MOC). For most physical crude and product assessments, the MOC window is the final 30 minutes of the trading day. During the window, bids and offers and trades are reported in real time through the Platts eWindow system. Traders can bid or offer any assessable cargo, and Platts editors use the sequence of bids, offers, and trades during the window to arrive at a single published assessment for the day. The window is deliberately narrow to ensure that the assessment reflects liquidity at the close rather than stale trades from the morning.

Because published Platts assessments feed directly into billions of dollars of physical supply contracts and OTC swaps, the MOC window is where some of the most intense short-term price formation happens in the oil market. A trader who wants to nudge an assessment upward can post a bid during the window; the bid has to be backed by real willingness to transact, but it shapes the editors' read of the market. Regulatory scrutiny of the MOC process has tightened since the mid-2010s after LIBOR and other assessment benchmarks came under investigation, and Platts publishes its methodology in detail. The MOC model is now imitated by Argus, OPIS, and every major commodity price reporting agency. When a wholesale oil supply contract says "Platts MOP" (Mean of Platts high and low) or "Platts MOC," it means the assessment produced by this window.

Oil and the US Dollar

Oil trades globally in US dollars for practical reasons: the dollar is the most liquid and freely convertible currency with the lowest transaction costs. A single currency makes international price comparison straightforward and enables efficient arbitrage. If the dollar weakens against consumption currencies, oil prices rise in dollar terms, and vice versa. Producers convert dollar revenues into any currency they want immediately.

Because the dollar itself is a moving target, headline oil prices can mislead about whether oil is genuinely more or less expensive in real terms. A useful sanity check is to price oil in gold, the longest-running unit of monetary value. The chart below plots WTI in dollars against the same WTI price expressed as the number of barrels you could buy with one troy ounce of gold. The two lines often move in opposite directions: from 2020 onward, dollar oil rose sharply while oil priced in gold actually got cheaper, because gold rose even faster than oil.

WTI Crude Oil Priced in Gold

The long-run average since the end of Bretton Woods is roughly fifteen barrels of WTI per ounce of gold. Periods well above that line, such as 2015 to 2017 and 2020 through 2025, mark eras when oil is cheap in hard-money terms. Periods well below, such as the 1970s oil shocks and the 2007 to 2008 super-cycle, mark eras when oil is genuinely expensive in real terms. Looked at this way, the high dollar prices of the early 2020s are a story about the dollar, not about oil.

Retail Price Differences

The primary driver of retail price differences between countries is government taxation, not crude oil costs. Dense European nations with mass transit alternatives can levy high fuel taxes. Low-density countries like the US, Canada, and Australia find it politically harder to tax automobile fuels. In 2026, European gasoline taxes can exceed $3 per gallon while US federal and state taxes combined average roughly $0.50 per gallon.

The above was updated in 2026. For the full original 2009 chapter, download the 1st edition 2009 PDF.